Not all mortgage brokers are the same. The word “broker” covers a wide range, from advisers with access to 30 or more lenders and no ownership ties to any of them, through to loan writers who work for a single bank and can only offer that bank’s products.

If you’re looking for a home loan in Perth and you’ve started researching your options, the independence question is worth asking early. It shapes which products you’ll be shown, how hard your broker will push lenders to sharpen their pricing, and whether you’re receiving genuinely unbiased mortgage advice built around your situation.

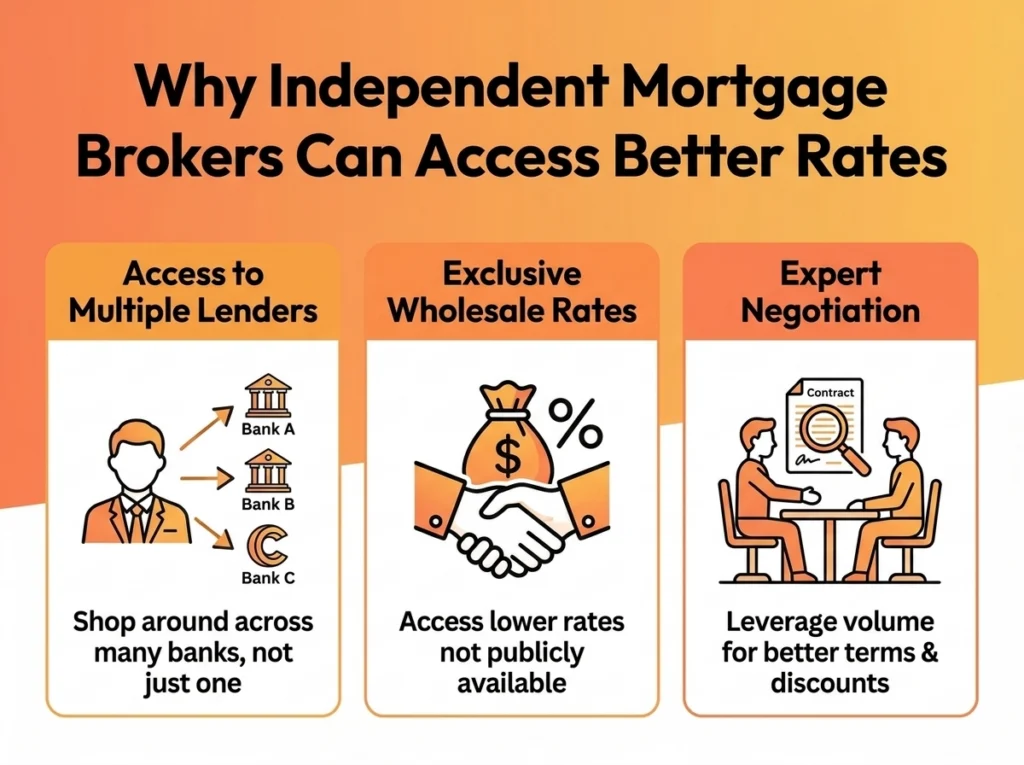

The short answer: independent brokers can access better rates because they have a wider lender panel, the ability to leverage lenders’ rate discretion, and no commercial reason to favour one lender over another. Here’s how each of those advantages actually works.

What “Independent” Actually Means

In Australian mortgage broking, “independent” isn’t a regulated term with a strict legal definition. In practice, a truly independent broker is one with:

- No ownership ties to a bank or financial institution — not employed by, part-owned by, or commercially aligned with any single lender

- An open lender panel — access to products across a broad range of lenders, not a curated shortlist influenced by commercial agreements

- Remuneration that doesn’t favour specific lenders — upfront and trail commissions are standard across the industry, but independent brokers don’t receive incentives to push one lender’s products over another’s

The contrast is with a bank-employed loan writer, who can only present that bank’s products, or a broker working within an aggregator model where commercial arrangements effectively limit the options they actively present.

In Perth’s mortgage market, that distinction matters. The gap between lenders on rate, fees, and loan features can be significant, and you only benefit from that competition if your broker is genuinely looking across the whole market.

The Panel Advantage: 30+ Lenders Competing for Your Business

A bank can only offer you its own loan products. An independent broker with a wide lender panel can show you what the market actually looks like.

At Strategic Mortgages, we have access to more than 30 lenders — the major banks alongside a broad range of non-bank lenders, credit unions, and specialist lenders. For a Perth borrower, that means comparing products across:

- Variable and fixed rate home loans

- Loan features (offset accounts, redraw facilities, split loans)

- Fee structures (application fees, ongoing fees, discharge fees)

- Serviceability assessments, which vary meaningfully between lenders

Not every lender suits every borrower. A first home buyer purchasing in Baldivis with a 10% deposit has different needs and different lender options than an investor refinancing in Wembley or a self-employed buyer in Fremantle. A wider panel creates a better match between your financial profile and the most suitable product.

It’s also worth noting that some competitive lenders operate primarily through brokers and don’t have a direct retail presence in Perth. A borrower going straight to a bank can’t access those products at all.

Negotiating Power: How Rate Discretion Works

Here’s something many Perth borrowers aren’t aware of: lenders have rate discretion.

The interest rate published on a lender’s website is a starting point, not a fixed offer. Lenders can, and regularly do, offer rates below their advertised pricing, particularly for borrowers with strong profiles (stable income, solid equity or deposit, clean credit history) and for brokers who bring consistent loan volume to that lender.

An independent broker with established lender relationships is positioned to use that discretion. The conversation with a lender isn’t simply “here’s a borrower, what’s your rate?” — it’s shaped by knowing which lenders are currently aggressive on pricing, which ones are hungry for new business, and what the realistic floor looks like for a given borrower profile.

That negotiating position is weaker if a broker works through a narrow panel or has commercial reasons to favour particular lenders. It’s stronger when the broker’s primary interest is finding the right outcome for you.

No broker can guarantee you a specific rate. What you’re offered depends on your financial profile, the lender’s current appetite, and prevailing market conditions. But the combination of lender competition and genuine negotiating leverage is what makes an independent broker’s position different from walking into a bank branch.

Ongoing Service: Annual Reviews and Rate Renegotiation

Independent brokers operating on a trail commission model have an ongoing commercial interest in keeping your loan competitive. Their commission continues as long as your loan is performing, which means it’s in their interest (as well as yours) to make sure you’re not paying more than you need to.

A good independent broker should contact you at least once a year to review your rate, assess whether your lender is still competitive, and explore whether refinancing makes sense. At Strategic Mortgages, that’s part of how we work. If your rate has drifted above what’s available in the current market, we’ll go back to your lender to renegotiate, or identify a better option elsewhere.

Perth borrowers who set-and-forget their loans can end up paying substantially more than necessary, particularly over a period of significant rate movement like the last few years. An independent broker with a stake in the ongoing relationship is better placed to catch and address that drift than a bank loan writer who moved on once your loan settled.

How Strategic Mortgages Approaches Independence

Strategic Mortgages is an independent Perth mortgage brokerage. We’re not owned by a bank, not commercially tied to any single lender, and our panel covers more than 30 lenders.

Our process starts with your situation — your income, deposit or equity position, goals, timeline — and works out from there. We’ll tell you when a deal is worth taking and when it isn’t. We’ll also tell you when refinancing doesn’t make financial sense, even if the initial rate comparison looks appealing on paper.

Trent Fleskens and the Strategic Mortgages team have been working with Perth buyers and property owners for over 25 years. Trent also hosts the Perth Property Show, a podcast covering the WA property market for buyers, investors, and homeowners who want a clearer picture of where things are heading.

Read what our clients say about working with us: Strategic Mortgages Reviews.

Questions to Ask Your Perth Mortgage Broker About Independence

Before you commit to working with a mortgage broker in Perth, these questions will give you a clear picture of how independent they actually are:

How many lenders are on your panel?

A broad panel — 30 or more — signals genuine market access. A short list warrants a follow-up question about why.

Are you owned by, or affiliated with, any bank or financial institution?

Bank-owned or bank-aligned brokers exist. The answer should be straightforward.

How are you paid, and does your commission vary by lender?

All Australian brokers are legally required to disclose their remuneration under the National Consumer Credit Protection Act. If commission rates vary significantly between lenders, ask how that influences recommendations.

What’s your process for selecting a lender for my situation?

A good broker should walk you through their methodology, not hand you a single recommendation without context.

Do you provide ongoing rate reviews after settlement?

This tells you whether the relationship ends when your loan settles or continues.

You’re entitled to clear answers to all of these. A broker who is evasive about their independence or commission structure isn’t someone you want managing a decision of this scale.

Experience Independent Mortgage Advice

The practical difference between going to a bank and working with a genuinely independent broker comes down to access to a broader market, access to rate negotiation, and access to ongoing support long after settlement.

If you’re buying a first home, refinancing, or adding an investment property in Perth, speak with our team of independent Perth mortgage brokers for unbiased advice. The initial conversation is free and obligation-free.

Frequently Asked Questions

What’s the difference between an independent mortgage broker and a bank?

A bank can only offer its own home loan products. An independent mortgage broker accesses products across a broad lender panel — typically 30 or more — and compares them to identify the right fit for your circumstances. The broker works for you, not the lender.

Can an independent broker access better rates than I can going direct?

Often, yes, though it depends on your financial profile and market conditions at the time. Independent brokers can leverage lender competition and rate discretion (lenders’ ability to offer below their advertised pricing) in ways most individual borrowers can’t replicate going direct. There are no guarantees, but the combination of market access and negotiating leverage is genuinely different from a direct bank approach.

How do independent mortgage brokers get paid?

In most cases, lenders pay brokers, not the borrower. Brokers receive an upfront commission when your loan settles and an ongoing trail commission while the loan remains active. Brokers are legally required to disclose their full commission structure. Ask any broker you speak with to explain their remuneration clearly before you proceed.

Will using a broker cost me more?

Generally, no. Broker-originated loans are typically priced the same as, or more competitively than, going direct to a lender. The broker’s commission comes out of the lender’s margin, not your pocket, and in most cases doesn’t appear as an additional cost to you. Confirm this with your broker at the outset.

How do I know if a mortgage broker is genuinely independent?

Ask directly: who owns your business, and do any commercial arrangements favour particular lenders? Check their lender panel size and ask how they select lenders for each client. Australian brokers are also subject to Best Interests Duty obligations. Ask how your broker applies this in practice and what that means for the advice you receive.

Ready to speak with an independent Perth mortgage broker? The team at Strategic Mortgages offers a free, obligation-free initial conversation — no paperwork, no pressure, just a clear picture of your options. Get in touch today.

Disclaimer: The information provided in this article is general in nature and does not constitute financial, tax, or legal advice. Individual circumstances vary. We recommend consulting with qualified professionals before making financial decisions.