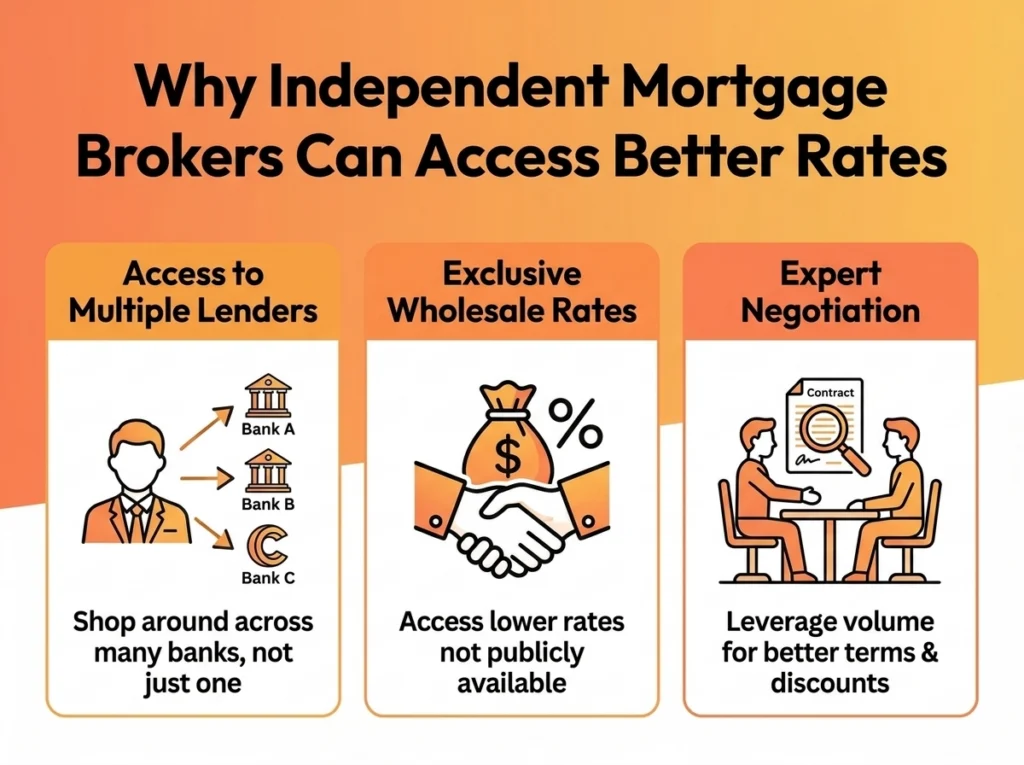

Not all mortgage brokers and loan writers have the same access to lenders. A bank loan writer can only discuss that bank’s products. Some brokerages also work from a narrower lender panel. A broad-panel mortgage broker can compare options across a larger group of lenders, which may give Perth borrowers a clearer view of rate, policy and feature differences.

The practical advantage is not a guaranteed lower rate. It is broader comparison, a better chance of matching lender policy to your circumstances, potential access to lender pricing discretion, and ongoing review after settlement.

If you are buying a home, refinancing or reviewing an investment loan in Perth, the lender panel question is worth asking early. It shapes which options are considered and how your broker explains the recommendation.

What a Broad Lender Panel Means

A broad lender panel gives a broker access to products from multiple lenders rather than one bank or a small shortlist. At Strategic Mortgages, we have access to more than 30 lenders, including major banks, non-bank lenders, credit unions and specialist lenders.

For a Perth borrower, that means comparing more than the headline interest rate. The right loan may depend on:

- variable and fixed rate options

- offset accounts, redraw facilities and split loan structures

- application, package, ongoing and discharge fees

- cash contribution or refinance offers where available

- serviceability assessment and credit policy

- turnaround times and settlement requirements

A wider panel does not mean every lender in Australia is available, and it does not mean the cheapest advertised rate is automatically the right fit. It does mean your broker can compare a broader set of options than a single bank can offer.

How Lender Competition Can Influence Pricing

Many lenders publish standard advertised rates, but those rates are not always the final pricing available to an approved borrower. Lenders may offer discretionary pricing based on the borrower profile, loan size, loan-to-value ratio, credit quality, employment position, property type and current appetite for new lending.

A broker who regularly deals with multiple lenders can request pricing, compare responses and identify where a lender may be more competitive for your circumstances. This can be especially useful when two lenders look similar on paper but differ on policy, fees or flexibility.

No broker can promise a specific rate. What you are offered depends on your financial position, lender policy, credit assessment and market conditions at the time. The value of a broad-panel approach is that more suitable options can be considered before a recommendation is made.

Why Policy Fit Matters as Much as Rate

The lowest advertised rate is not always the best practical option. A first home buyer in Baldivis with a 10% deposit may need a different lender approach from a self-employed borrower in Fremantle, an investor refinancing in Wembley or a household using a government guarantee scheme.

Lenders assess income, expenses, employment type, credit history, property type and deposit source differently. One lender may decline or limit a borrower where another lender has a clearer policy fit. A broker’s role is to compare both price and suitability, then explain why a particular option has been recommended.

Ongoing Reviews and Rate Renegotiation

Home loans can drift out of line with the market after settlement. Introductory offers expire, lender pricing changes and borrower equity positions improve over time. Regular reviews can help identify whether your current loan remains competitive.

At Strategic Mortgages, ongoing reviews are part of the service. If your rate has moved above comparable options, we can approach your current lender to request a review or compare refinance options elsewhere. Refinancing is not always worth doing once costs, effort and loan features are considered, so the comparison needs to be specific to your circumstances.

How Strategic Mortgages Compares Lenders

Strategic Mortgages is a Perth mortgage brokerage with access to a lender panel of more than 30 lenders. We are not owned by a bank, and our process starts with your situation: income, deposit or equity position, goals, timeline, property type and future plans.

Australian mortgage brokers must act in the consumer’s best interests when providing credit assistance. That means the recommendation should be based on your circumstances, not just a lender relationship or commission outcome. Brokers are also required to disclose how they are paid.

Trent Fleskens and the Strategic Mortgages team have worked with Perth buyers and property owners for more than 25 years. Trent also hosts the Perth Property Show, which covers the Western Australian property market for buyers, investors and homeowners.

You can also read Strategic Mortgages reviews from clients who have worked with the team.

Questions to Ask Your Perth Mortgage Broker

Before choosing a mortgage broker in Perth, ask questions that show how they compare lenders and manage conflicts:

- How many lenders are on your panel? A broader panel can provide more comparison points.

- Are you owned by, affiliated with or restricted by any lender? The answer should be direct and easy to understand.

- How are you paid? Ask for a clear explanation of upfront commission, trail commission and any fees payable by you.

- Does commission vary between lenders? If it does, ask how the broker manages that when making a recommendation.

- How do you decide which lenders to shortlist? A good broker should explain the policy, pricing and feature reasons for the shortlist.

- Do you provide reviews after settlement? This tells you whether the service continues after the loan settles.

- How do you apply the best interests duty? Ask what information they collect and how they document why a recommendation suits your circumstances.

Compare Your Perth Home Loan Options

The difference between going directly to one bank and working with a broad-panel broker is the range of options considered, the ability to compare lender policy, and the opportunity to request sharper pricing where available.

If you are buying a first home, refinancing or adding an investment property in Perth, speak with Strategic Mortgages. The initial conversation is free and obligation-free.

Frequently Asked Questions

What is the difference between a mortgage broker and a bank?

A bank can only offer its own home loan products. A mortgage broker can compare products across the lenders available on their panel, then explain which options may suit your circumstances and why.

Can a broker access more competitive rates than going direct?

Sometimes, but it depends on your financial profile, the lender, loan structure and market conditions. A broker may be able to request discretionary pricing or identify a lender that is more competitive for your circumstances. There are no guarantees.

How do mortgage brokers get paid?

In most cases, lenders pay brokers when a loan settles, and may also pay ongoing trail commission while the loan remains active. Brokers must disclose their remuneration. Ask any broker you speak with to explain how they are paid before you proceed.

Will using a broker cost me more?

Often there is no separate broker fee for residential home loan assistance because the broker is paid by the lender, but this should always be confirmed upfront. You should also compare the loan’s interest rate, fees, features and total costs before deciding.

How do I know whether a broker is comparing enough options?

Ask how many lenders are on the panel, which lenders were considered, which options were ruled out and why the final recommendation was selected. You are entitled to a clear explanation that connects the recommendation to your circumstances.

Disclaimer: The information provided in this article is general in nature and does not constitute financial, tax, or legal advice. Individual circumstances vary. We recommend consulting with qualified professionals before making financial decisions.