Cash flow is usually the first thing Perth investors ask about once they’ve found a property. An interest-only investment loan is one of the more common ways to manage it, but it’s also one of the more misunderstood loan structures on the market.

This guide covers how interest-only investment loans actually work, what lenders look for when assessing an application, and just as importantly, what happens once the interest-only period ends.

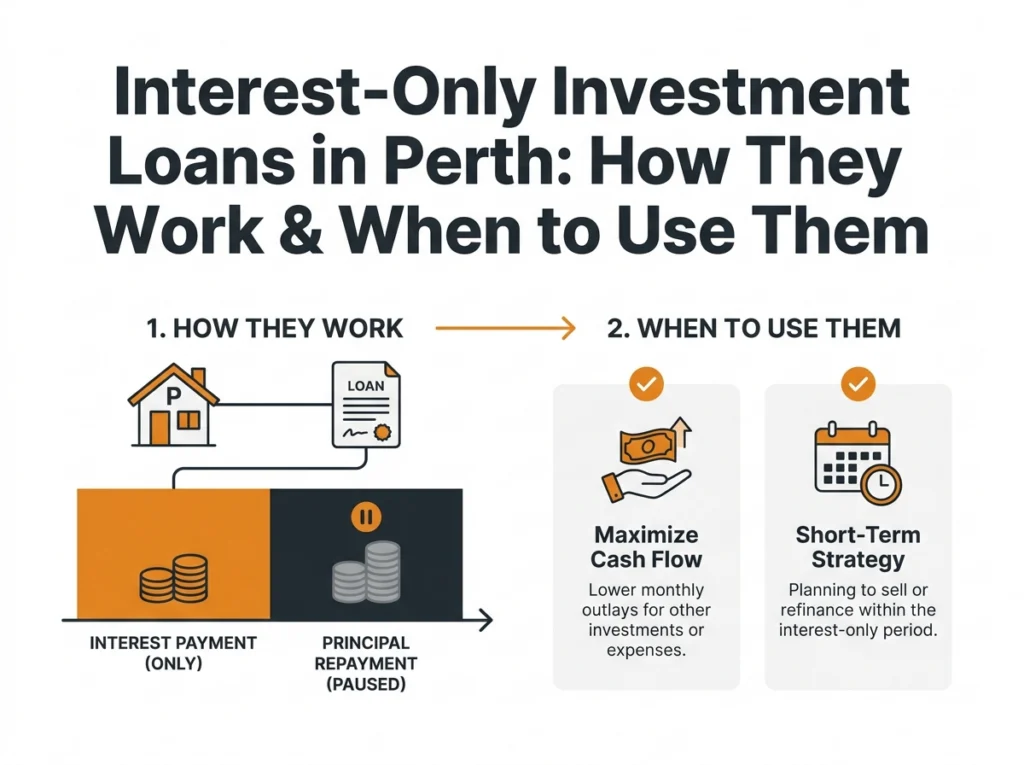

What Is an Interest-Only Investment Loan?

An interest-only investment loan lets you pay only the interest on the amount borrowed for a set period, typically one to five years. The loan balance itself stays the same throughout that period. Once it ends, the loan automatically reverts to principal-and-interest repayments, and your monthly repayment amount goes up. Lenders generally apply stricter serviceability checks to interest-only applications than they do to standard principal-and-interest loans, because the risk profile is different. It’s worth being clear-eyed about what this structure actually does: an interest-only loan doesn’t reduce your debt during the IO period, it manages your cash flow. Those are two different things, and mixing them up is where a lot of investors get caught out.

For a plain-English explainer on the mechanics, ASIC’s Moneysmart guide to interest-only home loans is a useful starting point. Not sure whether an interest-only structure fits your situation? Talk to an investment mortgage broker in Perth before you apply.

How Interest-Only Loans Work: The Numbers

The appeal of an interest-only loan comes down to monthly cash flow. Here’s a simplified comparison on a $500,000 investment loan, using an example rate of 6.50% p.a. for illustration only:

| Repayment type | Approximate monthly repayment | What’s happening to the loan balance |

|---|---|---|

| Interest-only | $2,708 | Stays at $500,000 |

| Principal & interest (30-year term) | $3,160 | Reduces gradually each month |

That’s roughly $452 a month staying in your pocket during the interest-only period rather than going toward the loan balance. These figures are illustrative only – actual rates, fees and repayments vary by lender and circumstances. Rates quoted are correct as at July 2026; verify current rates with your lender or broker.

How Long Can You Have an Interest-Only Period?

Interest-only periods on investment loans are typically available for one to five years, though this is lender-dependent – some offer shorter maximums, others will consider longer arrangements in specific circumstances. There’s no single fixed period across the market, so confirm the exact terms with your broker or lender before you commit.

Some lenders let you apply to extend an interest-only period as it approaches its end, though this isn’t guaranteed and depends on your circumstances, the property’s performance and the lender’s policy at the time.

Serviceability: How Lenders Assess Interest-Only Applications

Lenders don’t assess an interest-only application the same way they’d assess a standard principal-and-interest loan. Most calculate your serviceability based on the higher principal-and-interest repayment you’ll eventually face once the IO period ends, not the lower repayment you’re paying during it.

That approach exists because the lender needs to know you can afford the loan once it reverts. It’s one of the main reasons interest-only approval can be harder to secure than a standard investment loan for the same amount. We can’t guarantee approval either way – it always depends on individual serviceability assessment and full credit checks at application time.

A few factors typically carry more weight in an IO application:

- Your existing debt load, including any other interest-only loans

- How much of your rental income the lender counts toward serviceability (usually a portion, not the full amount)

- Your buffer against future rate rises, tested against the higher P&I repayment

When Might an Interest-Only Loan Suit a Perth Investor?

Perth’s rental market has been tight for some time. REIWA recorded a vacancy rate of 2.1% in June 2026, below the 2.5-3.5% range REIWA considers a balanced market. That doesn’t make the case for interest-only lending on its own, but it’s part of why cash flow management is front of mind for a lot of Perth investors right now. Interest-only structures tend to come up for a few common reasons:

- Managing cash flow while building a portfolio. Lower repayments can free up funds toward a deposit on the next property, depending on your broader lending strategy and serviceability across existing loans.

- Matching loan structure to investment timeframe. If the plan is to hold and sell later, some investors prefer to direct spare cash flow elsewhere rather than pay down a loan balance they intend to clear at sale.

- Smoothing a temporary income gap. Parental leave, a career change or a renovation period are examples where lower repayments may help, weighed against the higher repayment waiting at the end of the IO period.

What works for one portfolio can be the wrong call for another. This is worth talking through with a broker rather than assuming it’s the default choice for every investment property.

The Transition: What Happens When the Interest-Only Period Ends

This is the part of an interest-only loan that catches people off guard if they haven’t planned for it. When the IO period expires, the loan reverts to principal-and-interest repayments automatically – you don’t need to do anything for it to happen. Your monthly repayment increases from that point to cover both interest and principal.

Using the earlier example, that step-up could look like moving from roughly $2,708 a month to roughly $3,160 a month, an increase of around $452. The actual figure depends on the remaining loan term, the interest rate at the time and how much of the original IO period has passed.

Plan for this transition well before it happens, not in the final month. Options worth discussing with your broker in the lead-up include refinancing, requesting an extension, or adjusting your budget to absorb the higher repayment. Perth investors who review their loan structure three to six months out from the IO expiry date generally have more options than those who wait until the repayment actually changes.

Interest-Only Loans and Tax: What You Need to Know

Interest deductibility, negative gearing and how an interest-only structure interacts with your tax position are questions we hear often – and they’re not ones a mortgage broker is licensed to answer. Our role covers the loan itself: structure, rate, lender and serviceability. Whether an interest-only loan suits your tax position is a separate question that depends on your individual circumstances.

The ATO’s guidance on rental property deductions is a starting point for what applies generally. We recommend speaking with a qualified tax professional or accountant about your specific situation before deciding on a loan structure.

Should You Fix or Keep Variable on an Interest-Only Loan?

Fixed and variable rates both come with interest-only options on most lenders’ investment products. A variable rate gives you flexibility to make extra repayments or refinance without break costs. A fixed rate gives you certainty over what you’ll pay each month until the term ends. The right choice depends on your appetite for rate movement, how long you’re planning to hold the IO period, and current RBA conditions – worth raising with your broker before you lock in either option.

Frequently Asked Questions

Can I get an interest-only loan on an investment property in Perth?

Yes, most major and non-bank lenders offer interest-only investment loans, though approval depends on your individual serviceability and the lender’s current policy. Perth investors should expect a more detailed assessment for an IO application than for a standard principal-and-interest loan.

How long can an interest-only period last?

Interest-only periods are typically available for one to five years, though this is lender-dependent. At the end of the period, the loan generally reverts to principal-and-interest repayments unless you apply to extend the IO period or refinance beforehand.

Do interest-only loans cost more overall than principal-and-interest loans?

Over the life of the loan, an interest-only loan can mean more total interest paid, since the principal balance doesn’t reduce during the IO period. Whether that trade-off suits you depends on your cash flow needs and investment strategy – a broker can help you weigh it up.

What happens if I can’t afford the higher repayments once the interest-only period ends?

Plan for this well ahead of time. Options may include refinancing, requesting an extension, or adjusting your budget in advance. Talking to your broker three to six months before the IO period expires generally gives you the most options.

Is the interest on an investment loan tax deductible?

This depends on your individual circumstances and how the loan is used. We can’t provide tax advice – we recommend speaking with a qualified tax professional or accountant about how deductibility and negative gearing apply to your situation.

Do lenders require a bigger deposit for interest-only investment loans?

Not necessarily a bigger deposit, but many lenders apply tighter LVR (loan-to-value ratio) caps and stricter serviceability tests to interest-only applications. Some cap interest-only investment lending at 80% LVR or lower, though this varies by lender and is subject to change.

Ready to Talk About an Interest-Only Investment Loan?

If you’re building out a wider portfolio rather than a single purchase, our guide on structuring loans for a growing property portfolio covers how Perth investors sequence multiple purchases.

Considering an interest-only investment loan in Perth? Talk to the team at Strategic Mortgages Perth about your serviceability and structure options before you commit to a loan.

Speak to an investment mortgage broker in Perth.

Disclaimer: The information provided in this article is general in nature and does not constitute financial, tax, or legal advice. Individual circumstances vary. We recommend consulting with qualified professionals before making financial decisions.