Finding the right property in Perth’s market often means moving quickly, sometimes before your existing home has sold. This is exactly the situation a bridging loan is designed for. It can help you buy your next home while you’re still selling the one you’re in, without needing that sale to settle first.

This guide covers how it actually works in Western Australia, what lenders look for, and the risks worth understanding before you commit. It isn’t the right fit for everyone, so it’s worth going in with a clear picture rather than just the appeal of solving a timing problem.

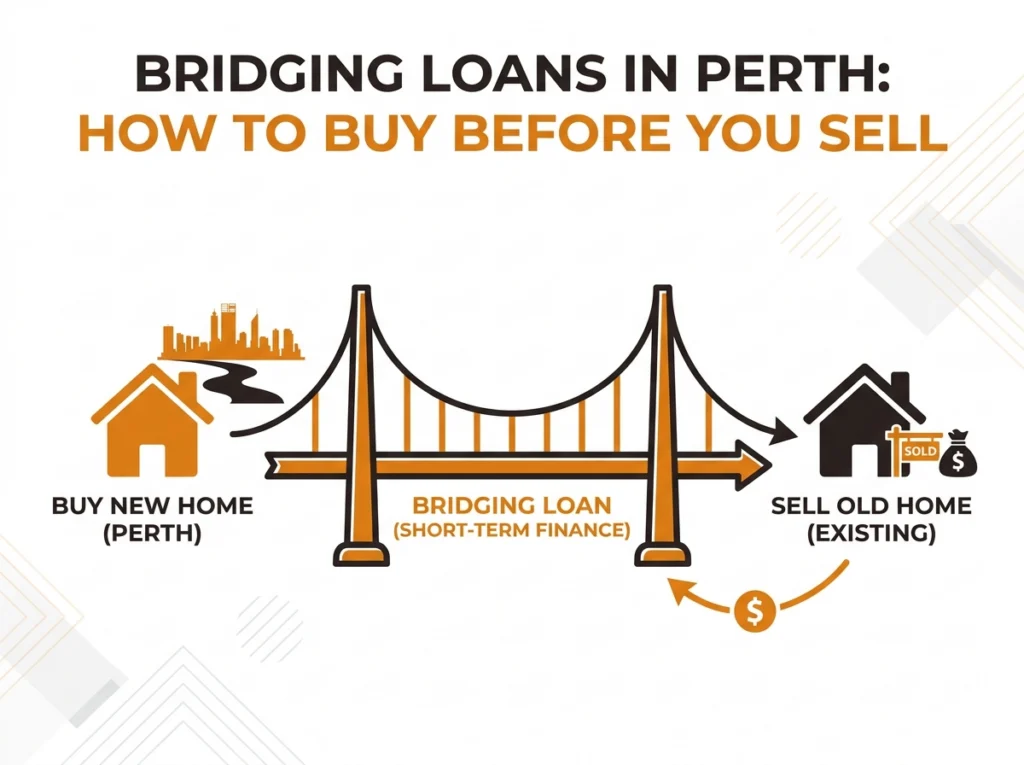

A bridging loan is short-term finance that covers the gap between buying a new property and selling your existing one. It typically combines your existing home loan and the loan needed for your new purchase into one “peak debt”, secured against both properties while you hold them. Once your existing home sells, the proceeds pay this down to an “end debt”, the ongoing loan amount on your new home. Bridging terms are typically around six to twelve months, depending on lender policy, and Perth lenders generally assess your ability to service that end debt, not just the temporary peak figure. Policies and timeframes can change.

What Is a Bridging Loan and How Does It Work?

MoneySmart defines bridging finance as short-term finance that covers the period between buying a new property and selling your existing one. There are two figures that matter here:

- Peak debt.Your combined debt while you hold both properties: what you still owe on your current home, plus what you need to borrow for the new one.

- End debt.What you’re left owing on your new home once your existing property sells and the proceeds are applied to the peak figure.

How interest is charged during this period depends on the lender. Some capitalise it, adding it to your loan balance rather than charging it as a monthly repayment. This can ease cash flow in the short term, but it means the debt can grow until your existing home sells.

Others require interest-only repayments on one or both loans for the duration. Canstar’s guide to bridging loans has more detail on how these structures typically differ.

How Much Can You Borrow?

How much you can access depends on three things. These are the combined equity across both properties, your ability to service the end debt once your current home sells, and the lender’s overall assessment.

Lenders typically want to see:

- A realistic sale price for your existing property, sometimes supported by a valuation or an active sales campaign.

- Sufficient equity across both properties to cover the peak figure.

- Confidence you can service the end debt on an ongoing basis, since this is what you’ll be left with long-term.

Because the whole arrangement relies on your current home actually selling, lenders build in a buffer. They generally take a conservative view of the expected sale price rather than the highest estimate on the market.

Eligibility: What Perth Lenders Look For

Not every lender offers this kind of finance, and criteria vary more here than with a standard home loan. In practice, Perth lenders will typically look at:

- Your equity position in your current home and the property you’re purchasing.

- Whether your current home is listed, under offer, or already sold subject to settlement. Some lenders require this before approving finance.

- Your income and ability to service the ongoing loan, assessed with a full credit check, not just the temporary combined figure.

- The valuation of both properties, arranged independently by the lender.

There’s also a Western Australia-specific timing factor worth knowing about. Western Australia has moved to mandatory electronic conveyancing, with property transactions settled and lodged electronically at Landgate, the state’s land titles registry. Settlement timeframes can still shift depending on how quickly your buyer’s finance and paperwork come together.

That timing directly affects how long you’ll be carrying the higher combined debt. It’s one more reason lenders build in a buffer rather than assuming a settlement date will hold exactly as planned. Pre-approval is an indication only, and final approval depends on valuation and a full credit assessment at the time of application, the same as any other home loan.

The Costs and Risks to Weigh Up

This type of finance solves a real timing problem, but it comes with trade-offs worth taking seriously.

- Rates and structures vary by lender. Some lenders charge the same rate as a standard home loan, others charge more, and most will move you to a higher rate if you don’t sell within the agreed term.

- If interest capitalises, it adds up. Where interest is added to the loan rather than paid monthly, the combined debt can grow noticeably over a six to twelve-month period.

- Your existing home may sell for less than expected, or take longer than planned. Either can leave you with a higher end debt than anticipated, or extension costs if the term needs to run longer.

- Both properties secure the loan while you hold them, so it’s worth understanding the full picture before committing to a purchase that depends on a sale you don’t yet control.

If you’re not sure whether the numbers stack up, a Perth mortgage broker can walk you through the risks honestly, not just the convenience of buying before you sell.

A Worked Example (Illustrative Only)

Say a Perth homeowner’s current property is valued at $700,000, with $280,000 owing on the mortgage. They find a new home for $820,000 and don’t have enough cash savings to cover the purchase outright.

Their combined peak debt while holding both properties would be approximately $1,100,000: the $280,000 still owed on the current home, plus the $820,000 needed for the new one. Interest on this amount may be added to the loan rather than paid monthly during the period both properties are held.

Once the current home sells, proceeds are used to pay out the original loan and selling costs. The remainder is applied to reduce the combined debt down to an ongoing end debt on the new home. The exact figure depends on the final sale price and selling costs. This is why a broker will typically model a conservative sale estimate rather than the top of the market.

This example is illustrative only. Actual figures depend on your properties, your lender, current interest rates and the eventual sale outcome.

Other Ways to Manage Buying Before Selling

A dedicated bridging structure isn’t the only way to manage buying and selling at the same time. Depending on your situation, it’s also worth considering:

- Selling first, then buying, which removes the timing risk but may mean temporary accommodation between settlements.

- A longer settlement or subject-to-sale offer on the property you’re buying, if the seller is open to it.

- Accessing equity in your current home to help fund a deposit, without a full bridging structure, if timing allows. Our guide to home equity loans in Perth covers this option in more detail.

A broker can talk through which of these fits your circumstances better than a generic comparison can. If the pressure is less about timing and more about simplifying repayments, our debt consolidation home loan guide is a better starting point.

How the Application Process Works

- Tell us about both properties. Your current home, the one you’re buying, and your expected timeline.

- We assess what’s realistic. This includes an estimate of your peak and end debt, and an honest view of whether this is the right fit.

- We compare lenders. Policies vary significantly between lenders, so we look across our panel rather than one bank’s offer.

- You choose a path. If it stacks up, we can help handle the application through to settlement on both properties.

Ready to Talk Through Your Timing?

If you’ve found your next home but haven’t sold your current one yet, Strategic Mortgages Perth can talk you through your options with no obligation. We can compare suitable bridging loan options across our lender panel and help you decide whether the timing risk is manageable for your situation.

Frequently Asked Questions

What is a bridging loan?

A bridging loan, sometimes called a bridging home loan, is short-term finance that lets you buy a new property before your existing one has sold. It combines your current mortgage and your new loan into a “peak debt”, which reduces to an “end debt” once your existing property sells and the proceeds are applied.

How does a bridging loan work?

It covers the period between settling on your new home and selling your existing one. Depending on the lender, interest during this period may be capitalised (added to the loan) or charged as interest-only repayments. Once your existing home sells, the proceeds pay down the loan, leaving your ongoing end debt.

How much equity do I need?

This depends on the lender and the value of both properties, but you’ll generally need enough combined equity to cover the peak figure with a reasonable buffer. A broker can assess your specific position.

What happens if my property doesn’t sell in time?

Most lenders set a term, often around six to twelve months, and may charge extension fees or move you to a different arrangement if your property hasn’t sold by then. Terms vary by lender and can change. This is one of the key risks to plan around before committing.

Is this type of finance available to everyone in Perth?

No. It’s a specialist product, and not every lender offers it. Eligibility depends on your equity, your income, the marketability of your current property, and the lender’s specific criteria. A broker can tell you which lenders are likely to consider your situation.

Disclaimer: The information provided in this article is general in nature and does not constitute financial, tax, or legal advice. Individual circumstances vary. We recommend consulting with qualified professionals before making financial decisions.