Most Perth homeowners know they should review their home loan at some point. Few actually get around to it.

The pattern is familiar. You set up your loan, life takes over, and four years slip by. Rates have moved. You’ve seen ads. But the review stays on the mental list, never quite making it to the calendar.

That gap — between when refinancing your Perth home loan could help and when you actually do something about it — can be costly. Not because the process is complicated. Because the triggers are easy to miss.

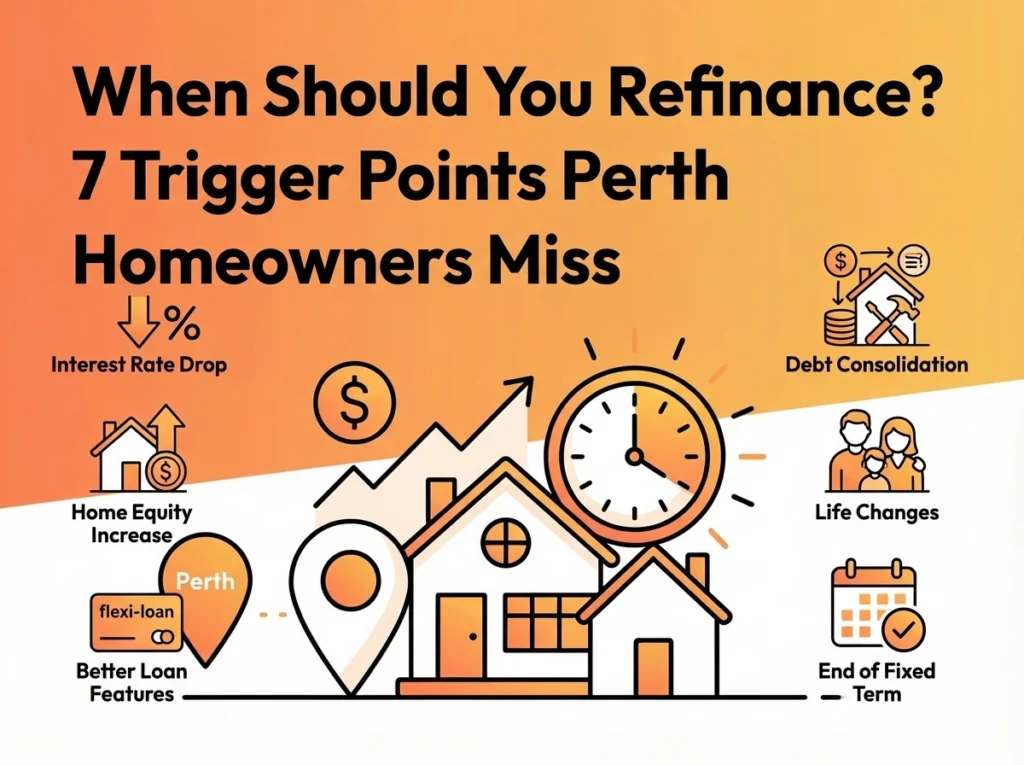

Here are seven situations that signal it’s worth having the conversation.

Trigger 1: Your Fixed Rate Period Is Ending

This one has a hard deadline. That makes it the most actionable trigger on the list.

When a fixed rate term expires, most lenders roll you onto their standard variable rate automatically. That rate is rarely their sharpest. If you don’t act before the rollover, you could end up paying more than you need to without noticing.

Start looking at your options 60 to 90 days before the expiry. That’s enough time to compare, apply, and settle without rushing. Your loan contract or most recent annual statement will show the date. Can’t find it? A broker can check in minutes.

Trigger 2: Interest Rates Have Dropped

A rate movement doesn’t automatically mean you should refinance. But a genuine gap between what you’re paying and what’s available in the market is worth a proper look.

As a rough guide: a difference of 0.5% or more on a remaining balance above $300,000 is generally worth assessing. On a $500,000 loan with 20 years left, a 0.5% reduction could meaningfully cut monthly repayments and the total interest saving over the life of the loan is often even more significant.

That said, any figure depends on your actual balance, term, and what rates you’d qualify for. A broker gives you a real-world number. A generic calculator gives you a starting point, and not much else.

Trigger 3: Your Property Value Has Increased

Perth’s property market has moved sharply over the past few years. REIWA data has shown consistent value growth across many suburbs, which means if you bought three or more years ago, your equity position may have improved more than you think.

More equity means a lower loan-to-value ratio (LVR). A lower LVR can open access to better rates, because many lenders reserve their keener pricing for borrowers with 20% or more equity. If you originally borrowed with a small deposit or at a lower purchase price, you may now qualify for products you couldn’t access before.

Worth checking.

Trigger 4: Your Income Has Increased

Higher income changes how lenders assess you. Full stop.

A salary increase, a role change, moving from casual to permanent, or starting to earn rental income — any of these shift your borrowing profile. That may open options at better rates or with lenders who are a better fit for where you are now.

The reverse matters too. If your income has dropped, refinancing becomes more complex — but acting sooner tends to produce better outcomes than waiting until repayments become unmanageable.

Trigger 5: Your Life Circumstances Have Changed

This is the one most people miss, because there’s no obvious financial number pointing at you.

Getting married, having a child, separating, changing careers, or planning to buy an investment property — any of these can affect which loan structure actually suits you. A product that made sense three years ago may not fit where you are now.

If something significant has changed in the past year or two, pair it with a mortgage review. The two conversations are more connected than they seem.

Trigger 6: You Haven’t Reviewed in Over 12 Months

Overdue. That’s the short answer.

Lenders update their pricing and product offerings regularly. A loan that was competitive 18 months ago may no longer be your best option, not because your loan changed, but because the market moved around it.

Most of the time a review confirms you’re in a reasonable position. Occasionally it finds a real opportunity. Either way, you know where you stand.

Annual mortgage reviews are something we recommend to every client at Strategic Mortgages Perth.

Trigger 7: You’ve Seen a Better Rate Advertised

This one works differently, because advertised rates can be misleading.

A headline rate in a bank ad or on a comparison site may not be available at your LVR, loan size, or income level. Products that look cheap on rate can also carry fees or restrictions that change the real cost when you look more closely.

That said, if you’re consistently seeing rates well below what you’re paying, don’t dismiss it. A broker can check your actual eligibility and give you a realistic picture of what you’d get, not what the ad promises.

Which Trigger Applies to You?

Refinancing isn’t right for every situation. Sometimes the costs outweigh the benefit. Sometimes the timing’s off. But you can’t know without looking.

If any of the seven triggers above sounds familiar, it’s worth a conversation. Our team helps Perth homeowners review their home loans every day — no pressure, just a clear picture of where you stand and what your options are.

Talk to a Perth mortgage broker and learn more about how to refinance home loan Perth options work today.

Frequently Asked Questions

How often should I review my Perth home loan?

Once a year is a reasonable rule. Lenders update their products and pricing regularly, and what was competitive 12 to 18 months ago may not be your best option today. An annual review with a broker takes less than an hour — and it either confirms you’re in good shape or turns up a better deal.

What does refinancing typically cost in Western Australia?

There may be a discharge fee from your existing lender, application or settlement fees with the new lender, and in some cases government fees for the title transfer. Whether those costs are worth it comes down to your loan balance, the rate improvement available, and how long you plan to stay in the loan. A broker can put together a real cost-benefit comparison for your situation. ASIC’s MoneySmart also has a mortgage switching calculator if you want a rough starting point.

Can I refinance if my property value has dropped?

It’s harder, but not always impossible. If your LVR has risen above 80%, you may need to pay Lenders Mortgage Insurance (LMI), or your options may be limited to lenders that accept higher LVR applications. Speak with a broker first — they’ll give you an honest read on what’s actually available.

Does refinancing affect my credit score?

Each formal credit application triggers a credit enquiry, which can temporarily affect your score. For this reason, it’s worth having a broker assess your realistic options before submitting formal applications. That way you’re only applying where there’s a solid chance of approval.

What’s the difference between fixed and variable when refinancing?

A fixed rate locks in your rate for a set period, usually one to five years, giving you predictable repayments. Variable moves with market conditions, so repayments can go up or down. Some borrowers split their loan: part fixed, part variable, for a bit of both. The right structure depends on your financial position and what you’re trying to achieve.

Disclaimer: The information provided in this article is general in nature and does not constitute financial, tax, or legal advice. Individual circumstances vary. We recommend consulting with qualified professionals before making financial decisions.